General Liability vs Professional Liability Insurance: What Small Business Owners Need to Know About Costs

Are You Paying Too Much for Business Insurance?

You’ve worked hard to build your business—but one unexpected lawsuit or mistake could cost you everything.

Here’s the real question: Do you actually have the right insurance coverage—or are you overpaying for the wrong one?

Many small business owners struggle to understand the difference between general liability vs professional liability insurance, and more importantly, how much business insurance really costs.

In this guide, we’ll break it all down in simple terms—no jargon, no confusion—so you can:

- Understand what each policy covers

- Know the average cost of business insurance

- Learn what affects your premiums

- Discover smart ways to save money

Let’s dive in.

What Is Business Insurance and Why Is It Important?

Business insurance is a financial safety net that protects your company from risks like lawsuits, accidents, and unexpected losses.

Without it, a single claim could lead to:

- Massive legal fees

- Property damage costs

- Loss of income

- Business shutdown

Why Small Businesses Need Insurance

Even if you’re running a small startup, risks are everywhere:

- A customer slips and falls in your store

- A client sues you for a mistake

- An employee gets injured

Insurance helps you survive these situations without draining your savings.

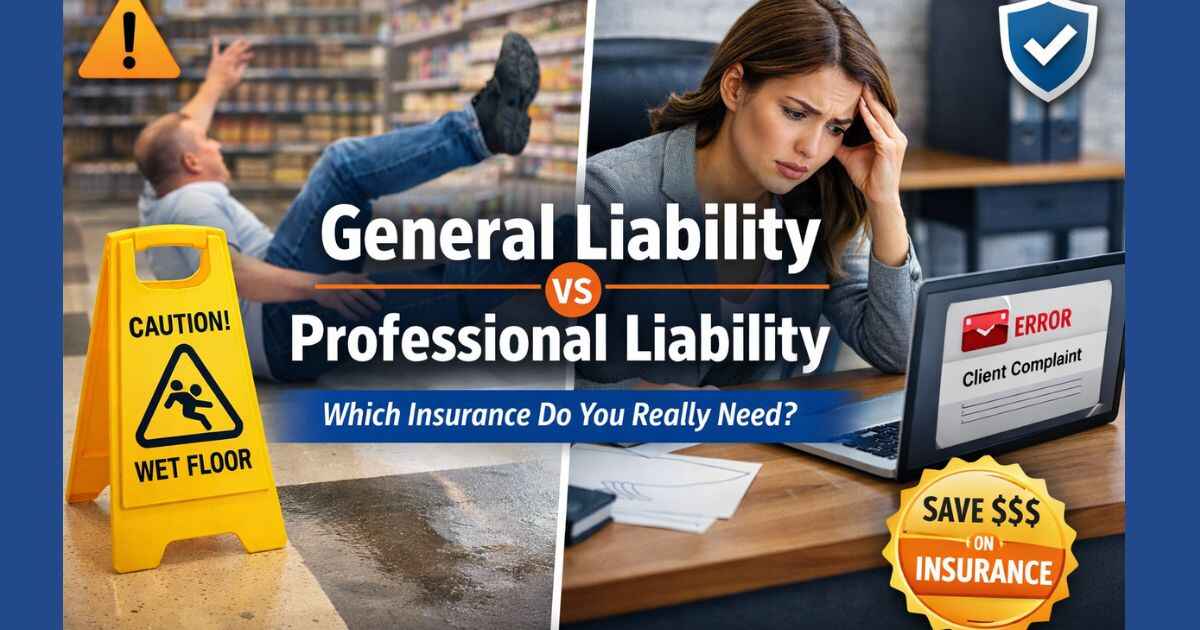

General Liability vs Professional Liability Insurance

This is where most business owners get confused. Let’s simplify it.

What Is General Liability Insurance?

General liability insurance protects your business from physical risks.

It Covers:

- Bodily injury (e.g., customer slips in your store)

- Property damage

- Advertising injuries (like copyright issues)

Example:

A customer visits your office, slips on a wet floor, and gets injured.

👉 General liability insurance covers medical expenses and legal fees.

What Is Professional Liability Insurance?

Also called Errors & Omissions (E&O) insurance, this covers service-related risks.

It Covers:

- Negligence claims

- Mistakes or errors in your service

- Missed deadlines causing financial loss

Example:

You’re a web designer, and your mistake causes a client to lose revenue.

👉 Professional liability insurance helps cover legal costs.

Key Differences at a Glance

| Feature | General Liability | Professional Liability |

|---|---|---|

| Covers | Physical risks | Service mistakes |

| Best for | Retail, restaurants | Consultants, freelancers |

| Claims type | Injuries, property damage | Financial loss due to errors |

👉 Bottom line:

Most businesses actually need both types of coverage.

How Much Is Business Insurance?

Let’s talk numbers—because this is what really matters.

Average Cost of Business Insurance

Here’s a breakdown of typical monthly costs in the U.S.:

1. General Liability Insurance

- $40 – $70 per month

- $500 – $800 per year

2. Professional Liability Insurance

- $50 – $100 per month

- $600 – $1,200 per year

3. Workers’ Compensation Insurance

- $70 – $200 per month (varies by payroll)

Combined Cost Estimate

For most small businesses:

👉 Total business insurance cost:

$500 – $3,000 per year

Factors Affecting Business Insurance Costs

Ever wondered why two businesses pay completely different premiums?

Here are the main factors affecting business insurance costs:

1. Industry Type

High-risk industries pay more.

- Construction → Higher premiums

- Consulting → Lower premiums

2. Business Location

Location plays a big role in pricing.

For example:

- Business insurance Colorado may cost more due to weather risks or regulations

- Urban areas often have higher liability risks

3. Business Size

More employees = higher risk.

- Larger payroll → higher workers’ comp costs

- More customers → higher liability exposure

4. Coverage Type and Limits

More coverage = higher cost.

- $1M policy → cheaper

- $2M policy → more expensive

5. Claims History

If you’ve filed claims before, insurers see you as risky.

👉 Result: Higher premiums

6. Revenue and Operations

Higher revenue businesses usually pay more because:

- More clients

- Bigger contracts

- Larger risks

Real-Life Scenario: Why Coverage Matters

Let’s say you run a digital marketing agency.

- A client sues you for poor results → Professional liability applies

- A visitor trips in your office → General liability applies

👉 Without both policies, you could be paying thousands out of pocket.

How to Save Money on Business Insurance

Now the part everyone cares about—saving money.

1. Bundle Policies

Combine general and professional liability into a Business Owner’s Policy (BOP).

👉 Saves up to 20%

2. Compare Insurance Quotes

Never go with the first option.

Get at least 3–5 quotes from different providers.

3. Increase Deductibles

Higher deductible = lower premium

👉 Just make sure you can afford it if needed.

4. Reduce Risks

Lower risk = lower cost.

You can:

- Install safety systems

- Train employees

- Maintain a clean workspace

5. Only Buy What You Need

Don’t overpay for unnecessary coverage.

Ask yourself:

👉 “What risks does my business actually face?”

6. Review Policies Annually

Your business grows—your insurance should adapt.

👉 For more tips on managing business expenses, check out

https://businessinsurancetalk.com

FAQs About Business Insurance Cost

1. How much is business insurance for a small business?

Most small businesses pay between $500 and $3,000 per year, depending on coverage and risk.

2. Is general liability insurance enough?

Not always.

If you provide services or advice, you also need professional liability insurance.

3. Why is professional liability more expensive?

Because lawsuits involving financial loss can be more complex and costly.

4. Can I run a business without insurance?

Technically yes—but it’s extremely risky and sometimes illegal depending on your state.

5. How can I lower my insurance premiums?

- Compare quotes

- Bundle policies

- Improve safety

- Avoid unnecessary coverage

Pro Tips from Insurance Experts

According to industry data:

- 40% of small businesses will face a liability claim within 10 years

- Legal defense costs can exceed $50,000 per claim

👉 That’s why having the right coverage isn’t optional—it’s essential.

Final Thoughts: Choose Smart, Not Cheap

Here’s the truth:

👉 Cheap insurance isn’t always good insurance.

Understanding general liability vs professional liability insurance helps you:

- Avoid financial disasters

- Protect your business reputation

- Save money in the long run

Protect Your Business Today

So, what’s your next step?

Ask yourself:

👉 Are you fully protected—or just guessing?

Take action now:

- Review your current coverage

- Compare multiple insurance quotes

- Talk to an expert if needed

Because one smart decision today can save your business tomorrow.